| The All-In-One Screener |

BALTIMORE (Stockpickr) -- Put down the 10-K filings and the stock screeners. It's time to take a break from the traditional methods of generating investment ideas. Instead, let the crowd do it for you. >>Buy These 5 Rocket Stocks to Beat the Market From hedge funds to individual investors, scores of market participants are turning to social media to figure out which stocks are worth watching. It's a concept that's known as "crowdsourcing," and it uses the masses to identify emerging trends in the market.

Crowdsourcing has long been a popular tool for the advertising industry, but it also makes a lot of sense as an investment tool. After all, the market is completely driven by the supply and demand, so it can be valuable to see what names are trending among the crowd.

While some fund managers are already trying to leverage social media resources like Twitter to find algorithmic trading opportunities, for most investors, crowdsourcing works best as a starting point for investors who want a starting point in their analysis. Today, we'll leverage the power of the crowd to take a look at some of the most active stocks on the market today. >>5 Blue-Chip Stocks to Trade for Gains These "most active" names are the most heavily-traded names on the market -- and often, uber-active names have some sort of a technical or fundamental catalyst driving investors' attention on shares. And when there's a big catalyst, there's often a trading opportunity.

Without further ado, here's a look at today's stocks. Micros Systems

Nearest Resistance: $68

Nearest Support: $67.80

Catalyst: Acquisition News

Shares of Micros Systems (MCRS) are up 3.4% this afternoon, following news that Oracle (ORCL) was planning on buying the mid-cap tech name for $68 per share. The news doesn't come as a total shock for shareholders of MCRS -- the rumor mill got this acquisition deal right earlier in the month, though the final numbers didn't hit until today.

Ultimately, the money has already been made on this name; shares of MCRS are sitting right below their $68 offer price this afternoon, a level that's acting like a fundamental resistance price for shares. If you didn't own MCRS before today, don't bother being a buyer here.

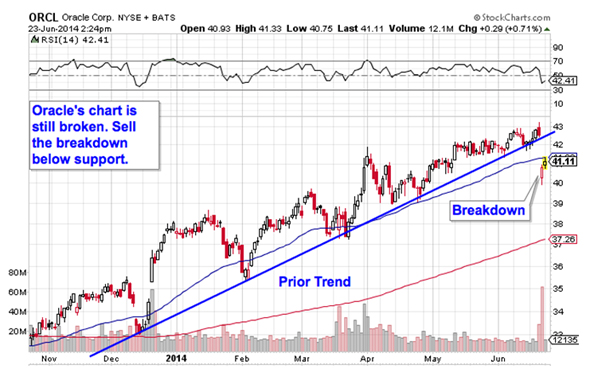

Oracle

Nearest Resistance: $42

Nearest Support: $40

Catalyst: MCRS Acquisition

The other side of the Micros Systems acquisition is Oracle, the enterprise software giant that's buying the smaller firm. Oracle's meaningful price action came at the end of last week with a conspicuous earnings miss. The miss was bad enough to shove shares down below the bottom of the uptrend that's been in play in shares since back in December.

Micros buy or not, Oracle's chart is broken right now. Advanced Micro Devices

Nearest Resistance: $4

Nearest Support: $3.70

Catalyst: Analyst Downgrade

Chip company Advanced Micro Devices (AMD) is down for a second straight day today, off just over 3% this afternoon following an analyst downgrade. AMD got sold off on Friday following news that high graphics card inventories could hamper sales in the quarter ahead, but today's downgrade by Pacific Crest is adding insult to injury for this mid-cap processor maker. Pacific Crest lowered AMD to "underperform".

Technically speaking, AMD is in "make or break mode" right now. Shares have been bouncing their way higher in a well-defined uptrend, but today's drop is threatening a breakdown below trendline support. If shares close below that lower trendline, it makes sense to join the sellers. To see these stocks in action, check out the at Most-Active Stocks portfolio on Stockpickr.

-- Written by Jonas Elmerraji in Baltimore.

RELATED LINKS:

>>5 Hated Earnings Stocks You Should Love

>>3 Stocks Spiking on Unusual Volume

>>5 Stocks Setting Up to Break Out

Follow Stockpickr on Twitter and become a fan on Facebook.

At the time of publication, author had no positions in the names mentioned.

Jonas Elmerraji, CMT, is a senior market analyst at Agora Financial in Baltimore and a contributor to TheStreet. Before that, he managed a portfolio of stocks for an investment advisory returned 15% in 2008. He has been featured in Forbes , Investor's Business Daily, and on CNBC.com. Jonas holds a degree in financial economics from UMBC and the Chartered Market Technician designation. Follow Jonas on Twitter @JonasElmerraji

The clear advantages of paying off your mortgage as quickly as possible have changed quite a bit over the past few years. The urgency to pay it off has somewhat diminished, as interest rates have plummeted to historical lows. It's no longer the black and white decision it was back when interest rates hovered between 6% and 9%, and even the 11% to 13% we saw a couple of decades ago. I am a big proponent of paying down that ugly mortgage beast as soon as is practical. But, before you go cutting a check to the bank, there is a pecking order of financial priorities you need to address before you consider tackling your mortgage. In order of importance, here are the places you need to put your financial attention first: Take The Cards Off The Table: Pay off all credit cards with high interest rates. Consider the huge discrepancy between credit cards with interest rates of 13% – 23%, and a 4% mortgage interest rate. In Case Of Emergency: You need to build an emergency fund, ideally 8-12 months of living expenses. Yes, today's job market is improving, but if you suddenly find yourself facing a layoff, you need to be prepared to sustain up to one year of living expenses. Build Up For Retirement: Are you able to make the maximum yearly contributions to your retirement accounts, 401K, IRA or an equivalent? Ask your accountant what the maximum allowable is for you and go for it! Get The Kids To School: Ah yes, the kids and college funds. Depending on how many children you have, how old they are, and what type of college enrollment expectation they have, you need to be making adequate contributions to those 529 plans or other college savings accounts. You May Live A Long Time: My mom is 97 this year, and my aunt just turned 100. So I am keenly aware that my money could run out before my health runs down. Another priority investment you need to be making each year is toward long-term health care insurance. It is not as costly when you start it in your 30's or 40's. But,! if you didn't get around to it till your 50's, it will take a hit out of your budget each month. Once you have paid out and paid off all of the above...you are ready to begin to slay the mortgage dragon with the remaining funds you have available. Next consideration is age. I believe that you should make efforts to pay off that mortgage by the time you plan to retire. There is something very freeing about the release of that last mortgage payment when you switch to a fixed income. Plus, chances are you will not need the mortgage interest deduction. One important note that many people don't realize is that when you are into years 20 through 30 of your mortgage payment, you are paying very little actual interest compared to what you paid in the early years. The banks have very cunningly structured mortgages so that they get a large portion of their money early on via interest sooner than later over the 30 years. But How Fast & How Much Should I Pay Down? I always suggest making that decision by counting backwards. If you want to retire and be mortgage free by age 65, then calculate how much extra you will have to pay monthly or yearly to pay it off by that date. There are numerous calculators online that will help you do this – Bankrate has a great one you can access here. Here's an example: You bought your home at age 45 with a 30 year loan at 5%. You are now 55 years old and you still owe $300,000 but plan to retire at 65. You are going to need to up your current payment of approximately $1,650 a month to approximately $2,650 a month till age 65. Not only will you get your mortgage paid off ten years sooner, you will have saved almost $78,000 in interest! The Motley Fool is a USA TODAY content partner offering financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

<SCRIPT language='JavaScript1.1! 'SRC="htt! p://ad.doubleclick.net/adj/N4538.USAToday/B2304017.8;abr=!ie;sz=550x300;ord=[timestamp]?"></SCRIPT><NOSCRIPT><AHREF="http://ad.doubleclick.net/jump/N4538.USAToday/B2304017.8;abr=!ie4;abr=!ie5;sz=550x300;ord=[timestamp]?"><IMGSRC="http://ad.doubleclick.net/ad/N4538.USAToday/B2304017.8;abr=!ie4;abr=!ie5;sz=550x300;ord=[timestamp]?" BORDER=0 WIDTH=550 HEIGHT=300ALT="Advertisement"></A></NOSCRIPT>

Currency funds manager Axel Merk warns the die of the dollar’s long-term decline has been cast, suggesting investors recognizing we’ve crossed this currency Rubicon may find salvation in a widely “misunderstood” euro. In a recent commentary, the chief investment officer of Merk Investments, which managers four currency-based funds, offers a variety of unflattering comparisons between U.S. monetary and fiscal management and that of the oft-maligned eurozone. The euro, he notes, bested the dollar two years ago in the midst of the eurozone crisis, and last year as well. U.S. monetary policy, with its emphasis on the purchase of Treasury and mortgage-backed securities, has kept rates low. But rising rates — to be expected as the Federal Reserve tapers its bond purchases — have been associated with a weakening dollar, Merk says. A greater problem, however, is our inability to afford positive real interest rates. “The biggest threat we face might be economic growth,” her writes, “because a stronger economy may warrant higher interest rates in order to contain rising inflationary pressures.” And if rates returned to their historic average of 5.6% between 1973 and 2012, the ensuing $1.2 trillion in interest expense (from our current $220 billion) would overwhelm the federal budget. The currency investor sharply criticized what he sees as the Yellen Fed’s abandonment of its price stability mandate, arguing the Fed actually wants inflation “to push up home prices … and to dilute the value of government debt.” Such a policy is a further blow to the long-term value of the dollar. In contrast, the “ugly duckling” euro, as he calls it, has not taken the Fed’s money printing approach. Whereas the U.S. has expanded its balance sheet by close to 360% since August 2008, the European Central Bank's balance sheet has expanded about 50% over the same time period. Moreover, “the cost of borrowing for weaker eurozone countries has been falling since August 2012,” he writes; the contraction in the spread between Spanish 10-year bond yields over the German benchmark from well over 6% to about 2% today adds an important source of stimulus, he says. Merk describes a number of efforts and ideas to weaken the value of the euro — which for structural and other reasons have been ineffective — which is further good news for euro currency investors. The eurozone has been “healing,” he says, noting that European flare-ups no longer trigger “contagion,” as in previous crises involving Cyprus and Spain. A sign of the improvement is the healthy development of hedge funds buying Greek banks and Spanish real estate — risk investments that, if they go wrong, will damage wealthy private investors rather than major European banks as in the past. The U.S., on the other hand, is saddled with a massive current account deficit, which, as he puts it, means it “needs to attract over 1 billion U.S. dollars every day to keep the currency from falling,” in contrast to internally financed eurozone budget deficits. That makes the U.S. vulnerable to bond vigilantes in the future, Merk warns. “If [the] bond market acts up the U.S. dollar might come under more pressure than the euro has ever seen," he concludes, "and would force policy makers to impose reforms.”

NEW YORK (CNNMoney) A bath in donkey's milk, the blood of children, tortoise scrotum soup -- the list of anti-aging treatments goes back centuries. No need to go that far. It turns out, the best kind of anti-aging treatment is inside one's own body, and the rich are taking advantage of it, exploring the latest research in new technologies, genome mapping and stem cell treatments. Among them is Oracle billionaire Larry Ellison, a large investor of the Ellison Medical Foundation, which supports research exploring the biology that underlies aging and age-related diseases. And there's billionaire Peter Nygård, who says he wants to live forever (or die trying), and has suggested he's found the keys to immortality in stem cell research. Some doctors agree that stem cells are a key part of chasing youth. "If you're a wealthy guy and haven't stored your stem cells, I think you're a total idiot," said Dr. Lionel Bissoon, a New York City physician who sees a number of stressed out, wealthy patients. They usually come to him with similar problems: "Fatigue, belly fat, erectile dysfunction, tiring very quickly ... all very common with my patients from Wall Street," Bissoon said. The short-term solution to those ailments, he says, is testosterone replacement -- which is relatively affordable at a few hundred dollars a pop -- and IV nutrition. For the long term he recommends stem cell storage, which works as a sort of rainy day insurance. The cells are extracted, preferably when the patient is on the younger side -- around 30 is said to be a good age -- and can then be used to boost an immune system or help to rebuild damaged organs later. Dr. Dipnarine Maharaj stores cells at his South Florida Bone Marrow Stem Cell Transplant Institute in Boynton Beach, Fla. "People are looking! and finding ways to be able to help them to live longer to spend the money they've earned," he said. "They spend their retirement going doctor to doctor, and if we can find ways to prevent that it would be good." His clinic sees executives under a lot of stress, a fast way to damage any immune system. He agrees that it's important to store cells before they become irreparably damaged. To collect and store stem cells at his clinic costs $15,000 for the initial extraction, which includes a year of storage. After that, storage costs $50 per month. Stem cells aren't the only high-end solution. Earlier this year, Malaysian billionaire Tan Sri Lim Kok Thay reportedly became one of the initial financial backers of a new genomics and cell therapy technology company called Human Longevity, dedicated to tackling age-related diseases and expanding the human life span. Another company, Singapore-based Scéil, says it's the first to transform human cells into nearly any tissue type in the body. "This technology has the potential to reverse, or even cure diseases and repair damaged tissues of your body," the company told CNNMoney in an email. Scéil attempts to obtain "a complete backup" of your genome from a skin sample and stores it for future use. The program costs $60,000 plus storage fees of $5,000 for 10 years, or $25,000 for a lifetime. "The aging process can be manipulated," said Sonia Arrison, author of 100 Plus: How the Coming Age of Longevity Will Change Everything, From Careers and Relationships to Family and Faith. "We're just at the beginning. There really is going to be a revolution ... it's going to be possible and not crazy at all to have a human life expectancy of 150 years." She said that it's already possible to use 3D printers to construct organs, and that process will only get faster and more accessible. But all that advancement won't be available to all -- at least not at first. "Obviously the rich will get it fi! rst," she! said, comparing 3D printed organ availability to cell phones, which were once cost prohibitive to the masses. Now, six billion of the world's seven billion people have one, according to a U.N. study. "It's how long is the timeline between the rich getting it and the poor getting it," she said. Dr. Anthony Atala, who runs the Wake Forest Institute for Regenerative Medicine in Winston-Salem, N.C., is committed to making sure those outside the 1% get fair access to such technologies, so that "printing" organs on demand becomes something everyone can do. "Part of the automation is making sure we lower the cost of these technologies," he said.

Related FED Wholesale Price Declines Suggest Slower Economy Fed's Beige Book from Jun. 4th, 2014 Information received since the Federal Open Market Committee met in April indicates that growth in economic activity has rebounded in recent months. Labor market indicators generally showed further improvement. The unemployment rate, though lower, remains elevated. Household spending appears to be rising moderately and business fixed investment resumed its advance, while the recovery in the housing sector remained slow. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee's longer-run objective, but longer-term inflation expectations have remained stable. Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and labor market conditions will continue to improve gradually, moving toward those the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term. The Committee currently judges that there is sufficient underlying strength in the broader economy to support ongoing improvement in labor market conditions. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in July, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $15 billion per month rather than $20 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $20 billion per month rather than $25 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee's sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee's dual mandate. The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee's expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases. To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy remains appropriate. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run. Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Stanley Fischer; Richard W. Fisher; Narayana Kocherlakota; Loretta J. Mester; Charles I. Plosser; Jerome H. Powell; and Daniel K. Tarullo. Posted-In: News Futures Federal Reserve Markets Press Releases © 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved. Most Popular Trulia Rumored To Acquire Move Why 'How To Train Your Dragon 2' Is Another DreamWorks Disappointment 5 Stocks To Consider During The 2014 World Cup UPDATE: Morgan Stanley Initiates Coverage On BlackBerry UPDATE: Morgan Stanley Reiterates On General Electric On News Of Siemens/MHI Offer Breakdown Of Amazon Phone Opportunity By SunTrust Related Articles (FED) Fed Statement From Jun. 17-18th, 2014 Meeting Wholesale Price Declines Suggest Slower Economy Fed's Beige Book from Jun. 4th, 2014 FOMC Minutes from Apr. 29-30th, 2014 Fed Meeting David Einhorn Gives His Opinion On Bernanke, Yellen And Monetary Policy Fed Rate Decision/Statement from Apr. 30th, 2014 Around the Web, We're Loving... Abercrombie Stems Bleeding Sales in Key Brand A Pristine Trading Plan for Intra-Day Trading

Shutterstock/Africa Studio We are all busy. Everyone is looking to save both time and money. The big question is when it's worth it to swap one for the other. A few years ago, I found myself very busy at work. During my precious hours at home, I wanted to be able to relax. While I had always enjoyed the satisfaction of cleaning, it was starting to become a hated chore. So I hired a cleaning company to come to my apartment once a month. At first I thought it was great -- after working my four eight-hour shifts over two days I loved coming home to see the carpet freshly vacuumed and the bathroom sparkling. But soon I began to resent the money I was spending. I had to spend time de-cluttering before the cleaners came and often found myself re-cleaning areas not done to my (admittedly neurotic) standards. I wasn't spending my added time with friends or sleeping -- I was mostly watching mindless TV on the couch. Plus, it turns out vacuuming can be a good stress-reliever that I was actually missing. I resumed cleaning my apartment and used the money savings to fund a future weekend getaway. The added bonus was I had something to look forward to and dream about during those long work shifts! Some people consider it a huge waste of money to pay someone to clean your home when you could do it yourself. Others feel the time they gain to spend on family, friends, work or hobbies makes the expense worth it. For me, it wasn't worth it. But for someone else, it might be. Is It Worth Driving for Cheap Gas? The average adult earns $42,700 per year. That's about $21 an hour if you crunch the numbers. Depending on where you live, your education and your profession, you may make more or less. So, one way to figure out whether a convenience is worth it is to calculate your hourly wage and price out the cost of doing certain activities. Now, assume that's what your time is worth (after all that's what you are valuing your time at by accepting that salary). Be sure to factor in the value of your time when assessing whether something is a bargain. For example, people often try to find the cheapest gas station to fill up their tank. But sometimes it's just not worth it. Consider that a gas station close to your house is charging 15 cents less per gallon than one 10 minutes away. If you have a 15-gallon tank you are saving $2.25. But you also spent 20 minutes - and some gas - driving to and from the gas station. If your time is valued at $21 per hour, 20 minutes is worth $7. That easily erases the $2.25 in savings. In fact, it's as if you are paying 31 cents more per gallon than you would at the closer gas station (this example also assumes you could be earning instead of going to the gas station). A bargain should be where you think you are getting a good deal even when you consider what your time is worth. So it might be worth it to go to that gas station if it is on the way to or from work or if you have other errands in the area. Shutterstock/Africa Studio We are all busy. Everyone is looking to save both time and money. The big question is when it's worth it to swap one for the other. A few years ago, I found myself very busy at work. During my precious hours at home, I wanted to be able to relax. While I had always enjoyed the satisfaction of cleaning, it was starting to become a hated chore. So I hired a cleaning company to come to my apartment once a month. At first I thought it was great -- after working my four eight-hour shifts over two days I loved coming home to see the carpet freshly vacuumed and the bathroom sparkling. But soon I began to resent the money I was spending. I had to spend time de-cluttering before the cleaners came and often found myself re-cleaning areas not done to my (admittedly neurotic) standards. I wasn't spending my added time with friends or sleeping -- I was mostly watching mindless TV on the couch. Plus, it turns out vacuuming can be a good stress-reliever that I was actually missing. I resumed cleaning my apartment and used the money savings to fund a future weekend getaway. The added bonus was I had something to look forward to and dream about during those long work shifts! Some people consider it a huge waste of money to pay someone to clean your home when you could do it yourself. Others feel the time they gain to spend on family, friends, work or hobbies makes the expense worth it. For me, it wasn't worth it. But for someone else, it might be. Is It Worth Driving for Cheap Gas? The average adult earns $42,700 per year. That's about $21 an hour if you crunch the numbers. Depending on where you live, your education and your profession, you may make more or less. So, one way to figure out whether a convenience is worth it is to calculate your hourly wage and price out the cost of doing certain activities. Now, assume that's what your time is worth (after all that's what you are valuing your time at by accepting that salary). Be sure to factor in the value of your time when assessing whether something is a bargain. For example, people often try to find the cheapest gas station to fill up their tank. But sometimes it's just not worth it. Consider that a gas station close to your house is charging 15 cents less per gallon than one 10 minutes away. If you have a 15-gallon tank you are saving $2.25. But you also spent 20 minutes - and some gas - driving to and from the gas station. If your time is valued at $21 per hour, 20 minutes is worth $7. That easily erases the $2.25 in savings. In fact, it's as if you are paying 31 cents more per gallon than you would at the closer gas station (this example also assumes you could be earning instead of going to the gas station). A bargain should be where you think you are getting a good deal even when you consider what your time is worth. So it might be worth it to go to that gas station if it is on the way to or from work or if you have other errands in the area.

WASHINGTON — Average U.S. rates on fixed mortgages rose this week but remained near historically low levels. Mortgage buyer Freddie Mac said Thursday the average rate for the 30-year loan increased to 4.33% from 4.28% last week. The average for the 15-year mortgage edged up to 3.35% from 3.33%. Mortgage rates have risen about a full percentage point since hitting record lows roughly a year ago. The increase was driven by speculation that the Federal Reserve would reduce its $85 billion-a-month bond purchases. Deeming the economy to be gaining strength, the Fed proceeded last month with planned reductions of its bond purchases, which have helped keep long-term interest rates low. STOCKS THURSDAY: How markets are doing The housing market is expected to deliver another year of solid gains, helped by an improving economy. Most economists expect home sales and prices to keep rising this year, but at a slower pace. They forecast that both will likely rise by about 5%, down from double-digit gains in 2013. Government data released Wednesday showed that U.S. home construction fell in January for a second straight month, but the weakness in both months reflected severe winter weather in many parts of the country. In a similar vein, U.S. homebuilders' confidence in the housing market declined sharply this month as the rough weather battering much of the nation keeps many would-be buyers at home, according to the National Association of Home Builders/Wells Fargo builder sentiment index issued Tuesday. To calculate average mortgage rates, Freddie Mac surveys lenders across the country between Monday and Wednesday each week. The average doesn't include extra fees, known as points, which most borrowers must pay to get the lowest rates. One point equals 1% of the loan amount. The average fee for a 30-year mortgage was unchanged at 0.7 point. The fee for a 15-year loan also remained at 0.7 point. The average rate on a one-year adjustable-rate mortgage rose to 2.57! % from 2.55%. The average fee declined to 0.3 point from 0.4 point. The average rate on a five-year adjustable mortgage increased to 3.08% from 3.05%. The fee held at 0.5 point.

Patrick T. Fallon/Bloomberg via Getty Images WASHINGTON -- U.S. consumer prices recorded their largest increase in more than a year in May as costs for a range of goods and services rose, pointing to a steady firming of inflation pressures. The Labor Department said Tuesday its Consumer Price Index increased 0.4 percent last month, with food prices posting their biggest rise since August 2011. The uptick in price pressures should comfort some Federal Reserve officials who had worried inflation was running too low. Still, a separate inflation gauge watched most closely by the Fed continues to run below the U.S. central bank's 2 percent target. Fed officials start a two-day policy meeting Tuesday. The Fed is expected to further trim its monthly bond buying program, but isn't seen raising interest rates until mid-2015. A separate report from the Commerce Department showed housing starts and permits fell in May, a sign that the housing recovery could remain in slow mode. Fed Chair Janet Yellen has warned that a protracted housing slowdown could undermine the economy. Groundbreaking for homes fell 6.5 percent to a seasonally adjusted annual pace of 1 million units in May. Permits declined 6.4 percent to a 991,000-unit pace, pulling back from the 1.06 million units touched in April. U.S. stock index futures turned negative on the data, while prices for U.S. Treasury debt fell. The dollar hit session highs versus the yen and the euro. "Medical care costs will help push inflation to 2 to 2.5 percent later this year. But the Fed could tolerate that," said Craig Dismuke, chief economic strategist at Vining Sparks in Memphis, Tennessee. Last month's increase in consumer prices was the largest since February 2013 and above economists' expectations for a 0.2 percent gain. It followed a 0.3 percent advance in April. In the 12 months through May, consumer prices increased 2.1 percent, the biggest rise since October 2012. That came on top of a 2 percent rise in April and was above economists' expectations for a year-on-year increase of 2 percent. It was the first back-to-back 2 percent rise in the year-on-year CPI since early 2012. Stripping out food and energy prices, the so-called core CPI rose 0.3 percent, the largest increase since August 2011. It had risen 0.2 percent in April. In the 12 months through May, the core CPI increased 2 percent. That was the biggest gain since February of last year and followed a 1.8 percent rise in April. Economists had forecast the core CPI rising 0.2 percent from April and 1.9 percent from a year-ago. Food prices increased 0.5 percent in May, rising for a fifth consecutive month. Prices for meat, dairy, fruit and vegetables rose. Poultry and fish prices also increased as did the cost of eggs. Gasoline prices increased 0.7 percent. Prices for electricity also rose after declining in the prior month. The core CPI was lifted by a 0.3 percent rise in rent. There were also increases in medical care costs, apparel, new cars prices and airline fares. -. Patrick T. Fallon/Bloomberg via Getty Images WASHINGTON -- U.S. consumer prices recorded their largest increase in more than a year in May as costs for a range of goods and services rose, pointing to a steady firming of inflation pressures. The Labor Department said Tuesday its Consumer Price Index increased 0.4 percent last month, with food prices posting their biggest rise since August 2011. The uptick in price pressures should comfort some Federal Reserve officials who had worried inflation was running too low. Still, a separate inflation gauge watched most closely by the Fed continues to run below the U.S. central bank's 2 percent target. Fed officials start a two-day policy meeting Tuesday. The Fed is expected to further trim its monthly bond buying program, but isn't seen raising interest rates until mid-2015. A separate report from the Commerce Department showed housing starts and permits fell in May, a sign that the housing recovery could remain in slow mode. Fed Chair Janet Yellen has warned that a protracted housing slowdown could undermine the economy. Groundbreaking for homes fell 6.5 percent to a seasonally adjusted annual pace of 1 million units in May. Permits declined 6.4 percent to a 991,000-unit pace, pulling back from the 1.06 million units touched in April. U.S. stock index futures turned negative on the data, while prices for U.S. Treasury debt fell. The dollar hit session highs versus the yen and the euro. "Medical care costs will help push inflation to 2 to 2.5 percent later this year. But the Fed could tolerate that," said Craig Dismuke, chief economic strategist at Vining Sparks in Memphis, Tennessee. Last month's increase in consumer prices was the largest since February 2013 and above economists' expectations for a 0.2 percent gain. It followed a 0.3 percent advance in April. In the 12 months through May, consumer prices increased 2.1 percent, the biggest rise since October 2012. That came on top of a 2 percent rise in April and was above economists' expectations for a year-on-year increase of 2 percent. It was the first back-to-back 2 percent rise in the year-on-year CPI since early 2012. Stripping out food and energy prices, the so-called core CPI rose 0.3 percent, the largest increase since August 2011. It had risen 0.2 percent in April. In the 12 months through May, the core CPI increased 2 percent. That was the biggest gain since February of last year and followed a 1.8 percent rise in April. Economists had forecast the core CPI rising 0.2 percent from April and 1.9 percent from a year-ago. Food prices increased 0.5 percent in May, rising for a fifth consecutive month. Prices for meat, dairy, fruit and vegetables rose. Poultry and fish prices also increased as did the cost of eggs. Gasoline prices increased 0.7 percent. Prices for electricity also rose after declining in the prior month. The core CPI was lifted by a 0.3 percent rise in rent. There were also increases in medical care costs, apparel, new cars prices and airline fares. -.

See the new Hot or Not LONDON (CNNMoney) Hot or Not, an online platform where people rate the attractiveness of participants, took the Internet by storm over a decade ago. Now Hot or Not's creators have relaunched the dating app to help people connect with the hottest people in their areas. The updated Hot or Not app encourages people to vote on the most attractive (and least attractive) users, then gives users a popularity score and compiles a 'Hot List' to show in real-time where the most babelicious people are each neighborhood. The app is designed to take the guesswork out of tracking down good-looking people. For example, concert goers using the app will be able to check their iPhones to see whether highly rated 'hot people' are at the bar or near the stage. Users can also chat through the app, provided they rate one another as 'hot'. "Since 2000, the Hot or Not brand has been an inspiration behind some of the most popular platforms and products currently available to consumers including Facebook (FB, Tech30) and YouTube," said Andrey Andreev, CEO of Hot or Not. "With the addition of 'Hot Lists' ... we are bringing an elevated and more exciting version of this iconic brand to a new generation of users." But the app is not for the faint of heart. Online daters can be ruthless in their assessment of people's physical attractiveness. Each individual will have a "hot rating" attached to their profile, which is decided by voting. Needless to say, some users may not be happy with their results. App lets girls anonymously ! rate guys The app currently has over 10 million users in the United States and is pitting itself against other popular dating apps it helped spawn, included Tinder. The company behind the app -- London-based Badoo -- would not reveal user numbers in other markets, though the app is available in over 30 languages. The Hot or Not mobile app originally launched in May 2013.

Justin Sullivan/Getty Images NEW YORK and DETROIT -- U.S. banks looking to get in on a booming market for financing new-car sales have run into a formidable competitor: the auto manufacturers themselves. Financing arms of car companies, including Toyota Motor (TM), Honda Motor (HMC) and Ford Motor (F), made half of all new U.S. car loans in the first quarter, up from 37 percent a year earlier and the largest percentage of the market in four years, according to credit data firm Experian (EXPR). These companies also write the vast majority of leases, which contributed a record 26 percent of new car sales in the quarter, up from 23 percent last year and 20 percent in 2012. The financing arms are providing subsidies from the manufacturers, lowering monthly payments and extending loan terms to make it easier for buyers to drive away in a shiny, new vehicle. As a result, major banks are increasingly moving into riskier parts of the market to make loans. U.S. Bancorp (USB), for example, for the first time ever decided to start financing used cars, an area of the market that the automakers' finance companies have little interest in. It also started offering loans to less creditworthy borrowers. And Wells Fargo (WFC) has been leveraging off a nationwide deal with General Motors (GM) to provide loans subsidized by the No. 1 U.S. automaker. Wells sees this as a way to gain more of the used car loan business at GM dealerships. The aggressive push by car companies is beginning to raise questions among industry analysts and consultants about whether it is sustainable. If interest rates rise, the automakers could find the incentives too costly unless they are prepared to take a hit to profits -- with any pullback in the deals being offered customers running the risk of hurting demand. And, if used car prices weaken, the financing units could be hit with losses on vehicles coming back from leases and repossessions. The automakers' financing companies are doing substantially more than they were just a year or two ago, said April Ancira, vice president in the San Antonio office of Ancira Motor, a Texas-based group with 11 dealerships selling GM, Nissan, Fiat, Chrysler, VW and Ford cars. "They're being very aggressive with incentives," Ancira said. Pete Carey, vice president for sales at Toyota Financial Services, said incentives are playing a bigger role as automakers look to stand out in a crowded market where the basic quality of cars is uniformly good. "We're at a point in the industry that we're spending as much as we've ever spent," Carey said. The strategy is currently paying off in spades for automakers. All the major automakers posted healthy profits in the first quarter. U.S. car sales rebounded in May to an annualized rate of 16.8 million vehicles, against 15.6 million for all of last year. Sales were only 10.4 million in 2009 as the recession crushed demand. Outstanding U.S. loans on new cars totaled $811 billion at the end of March, up 11.6 percent from a year earlier, according to Experian. Fears of Used-Car Glut The automakers are in a position to offer the deals because their cost of borrowing has gone down as their balance sheets have improved and as bond investors have lined up to buy securities backed by loans and leases. But they risk sweetening the deals so much that it starts to cut into their profit margins. In a few years time, as the leased vehicles are returned, the strategy could lead to a glut in the used-car market. If a car turns out to be worth less at the end of a lease than projected, the finance company will take a loss on the lease, said Jim Ziegler, a consultant to car dealers. "It appears as a profit until they get the car back," Ziegler said. Analysts at Moody's Investors Service said car resale values at the end of leases have so far tended to be higher than assumed, resulting in double-digit gains for finance companies and lease investors. But the gains have started to decelerate to single-digits now and they expect to see that downward pressure continue this year. "There is still room for used car prices to decline before we see any losses," said Aron Bergman, of Moody's. But, he added, "the gains are going down." Sweet Subsidies The average monthly lease payment for the most-leased car in America, the Honda Civic, was $251 in the first quarter, according to Experian. But when Jonathan Stierwald, a Minnesota resident, wanted to lease a car for his nephew, he found Mike Piazza Honda in Pennsylvania willing to lease him the car for three years for just $80 a month. He flew there to get the deal. The lease was financed by Honda's finance arm. The details of the deal could not be determined. A salesman at the Langhorne, Pennsylvania dealership, which is owned by Piazza, the former All-Star baseball catcher, said factors such as a high credit score and higher down-payment may have helped. Honda representative Steve Kinkade said the dealership could have added its own incentives on top of the company's promotions. Honda, which was fifth in U.S. auto sales in the first five months of the year, increased its average subsidy per leased car by 26 percent to $1,476 in that period from a year earlier, according to Edmunds.com. Kinkade said the company is pleased with how its finance unit has paced its leasing to drive sales without too many of the cars later coming onto the used car market and depressing prices. Others are liberally using subsidies, too. Toyota subsidized 92 percent of its U.S. leases in its fiscal year ending in March, up from 82 percent the year before. "We can get fairly aggressive with pricing or payments, depending on what we anticipate the used market to look like," Toyota's Carey said. Auto industry analysts and consultants said they did not think the situation was getting out of hand just yet. The average incentive per car sold so far this year was $2,918, up slightly from $2,825 a year earlier and just under 10 percent of the average transaction price, according to J.D. Power & Associates data. Banks In Used-Car Lots Automaker finance arms are also offering loans at interest rates as low as zero percent. And, they are taking on more loans to borrowers with subprime credit ratings, according to data from Experian. The length of loans is also increasing. Lenders granted one-in-four new car buyers more than six years to repay in the first quarter, up from one-in-five a year earlier, the figures show. The average monthly payment on new car loans was $474 in the first quarter, only $15 more than a year earlier, even as the average amount financed rose by $964 to a record $27,612. Unable to compete, some banks are in retreat. Ally Financial (ALLY), which was once GM's financing arm but is now on its own, increased its financing of used car purchases by 14 percent in the first quarter from a year earlier, but its new car lending declined so much that it made 6 percent fewer auto loans in total. U.S. Bancorp estimated that used cars will eventually make up 40 percent of its auto loans after doing none in the past. Consumers with "nonprime" credit scores, defined as below 675, will account for 15 percent of U.S. Bancorp's portfolio, compared with none previously. Not that the opportunity in the used car market isn't also large -- in terms of numbers of vehicles sold the used car market is more than twice the size of the new-car market. Tom Wolfe, executive vice president of consumer credit solutions at Wells Fargo, said its partnership with GM improves its ties with dealers and that for every subsidized new car loan it makes for GM at a dealer it will pick up three used-car loans. Wells Fargo is the largest U.S. used-car lender with a 7.1 percent market share, according to Experian. Wolfe said customers who borrow to buy a used car so that they can get to and from work are good credit risks. -. Justin Sullivan/Getty Images NEW YORK and DETROIT -- U.S. banks looking to get in on a booming market for financing new-car sales have run into a formidable competitor: the auto manufacturers themselves. Financing arms of car companies, including Toyota Motor (TM), Honda Motor (HMC) and Ford Motor (F), made half of all new U.S. car loans in the first quarter, up from 37 percent a year earlier and the largest percentage of the market in four years, according to credit data firm Experian (EXPR). These companies also write the vast majority of leases, which contributed a record 26 percent of new car sales in the quarter, up from 23 percent last year and 20 percent in 2012. The financing arms are providing subsidies from the manufacturers, lowering monthly payments and extending loan terms to make it easier for buyers to drive away in a shiny, new vehicle. As a result, major banks are increasingly moving into riskier parts of the market to make loans. U.S. Bancorp (USB), for example, for the first time ever decided to start financing used cars, an area of the market that the automakers' finance companies have little interest in. It also started offering loans to less creditworthy borrowers. And Wells Fargo (WFC) has been leveraging off a nationwide deal with General Motors (GM) to provide loans subsidized by the No. 1 U.S. automaker. Wells sees this as a way to gain more of the used car loan business at GM dealerships. The aggressive push by car companies is beginning to raise questions among industry analysts and consultants about whether it is sustainable. If interest rates rise, the automakers could find the incentives too costly unless they are prepared to take a hit to profits -- with any pullback in the deals being offered customers running the risk of hurting demand. And, if used car prices weaken, the financing units could be hit with losses on vehicles coming back from leases and repossessions. The automakers' financing companies are doing substantially more than they were just a year or two ago, said April Ancira, vice president in the San Antonio office of Ancira Motor, a Texas-based group with 11 dealerships selling GM, Nissan, Fiat, Chrysler, VW and Ford cars. "They're being very aggressive with incentives," Ancira said. Pete Carey, vice president for sales at Toyota Financial Services, said incentives are playing a bigger role as automakers look to stand out in a crowded market where the basic quality of cars is uniformly good. "We're at a point in the industry that we're spending as much as we've ever spent," Carey said. The strategy is currently paying off in spades for automakers. All the major automakers posted healthy profits in the first quarter. U.S. car sales rebounded in May to an annualized rate of 16.8 million vehicles, against 15.6 million for all of last year. Sales were only 10.4 million in 2009 as the recession crushed demand. Outstanding U.S. loans on new cars totaled $811 billion at the end of March, up 11.6 percent from a year earlier, according to Experian. Fears of Used-Car Glut The automakers are in a position to offer the deals because their cost of borrowing has gone down as their balance sheets have improved and as bond investors have lined up to buy securities backed by loans and leases. But they risk sweetening the deals so much that it starts to cut into their profit margins. In a few years time, as the leased vehicles are returned, the strategy could lead to a glut in the used-car market. If a car turns out to be worth less at the end of a lease than projected, the finance company will take a loss on the lease, said Jim Ziegler, a consultant to car dealers. "It appears as a profit until they get the car back," Ziegler said. Analysts at Moody's Investors Service said car resale values at the end of leases have so far tended to be higher than assumed, resulting in double-digit gains for finance companies and lease investors. But the gains have started to decelerate to single-digits now and they expect to see that downward pressure continue this year. "There is still room for used car prices to decline before we see any losses," said Aron Bergman, of Moody's. But, he added, "the gains are going down." Sweet Subsidies The average monthly lease payment for the most-leased car in America, the Honda Civic, was $251 in the first quarter, according to Experian. But when Jonathan Stierwald, a Minnesota resident, wanted to lease a car for his nephew, he found Mike Piazza Honda in Pennsylvania willing to lease him the car for three years for just $80 a month. He flew there to get the deal. The lease was financed by Honda's finance arm. The details of the deal could not be determined. A salesman at the Langhorne, Pennsylvania dealership, which is owned by Piazza, the former All-Star baseball catcher, said factors such as a high credit score and higher down-payment may have helped. Honda representative Steve Kinkade said the dealership could have added its own incentives on top of the company's promotions. Honda, which was fifth in U.S. auto sales in the first five months of the year, increased its average subsidy per leased car by 26 percent to $1,476 in that period from a year earlier, according to Edmunds.com. Kinkade said the company is pleased with how its finance unit has paced its leasing to drive sales without too many of the cars later coming onto the used car market and depressing prices. Others are liberally using subsidies, too. Toyota subsidized 92 percent of its U.S. leases in its fiscal year ending in March, up from 82 percent the year before. "We can get fairly aggressive with pricing or payments, depending on what we anticipate the used market to look like," Toyota's Carey said. Auto industry analysts and consultants said they did not think the situation was getting out of hand just yet. The average incentive per car sold so far this year was $2,918, up slightly from $2,825 a year earlier and just under 10 percent of the average transaction price, according to J.D. Power & Associates data. Banks In Used-Car Lots Automaker finance arms are also offering loans at interest rates as low as zero percent. And, they are taking on more loans to borrowers with subprime credit ratings, according to data from Experian. The length of loans is also increasing. Lenders granted one-in-four new car buyers more than six years to repay in the first quarter, up from one-in-five a year earlier, the figures show. The average monthly payment on new car loans was $474 in the first quarter, only $15 more than a year earlier, even as the average amount financed rose by $964 to a record $27,612. Unable to compete, some banks are in retreat. Ally Financial (ALLY), which was once GM's financing arm but is now on its own, increased its financing of used car purchases by 14 percent in the first quarter from a year earlier, but its new car lending declined so much that it made 6 percent fewer auto loans in total. U.S. Bancorp estimated that used cars will eventually make up 40 percent of its auto loans after doing none in the past. Consumers with "nonprime" credit scores, defined as below 675, will account for 15 percent of U.S. Bancorp's portfolio, compared with none previously. Not that the opportunity in the used car market isn't also large -- in terms of numbers of vehicles sold the used car market is more than twice the size of the new-car market. Tom Wolfe, executive vice president of consumer credit solutions at Wells Fargo, said its partnership with GM improves its ties with dealers and that for every subsidized new car loan it makes for GM at a dealer it will pick up three used-car loans. Wells Fargo is the largest U.S. used-car lender with a 7.1 percent market share, according to Experian. Wolfe said customers who borrow to buy a used car so that they can get to and from work are good credit risks. -.

Graco is recalling nearly 3.8 million car safety seats because children can be trapped, but is refusing to recall seven other infant seat models, according to a National Highway Traffic Safety Administration recall notice. n the seats being recalled, the buckles may not unlatch, making it difficult to remove the child from the seat. That increases the risk of injury in a crash, fire or other emergency when a speedy exit from the vehicle is required. "NHTSA's investigation will remain open pending its evaluation of the Graco recall and until the Agency's consideration of the review of the seven remaining seat models is completed," the agency said in a statement. That means the agency and company will continue to negotiate on whether a recall is warranted for the SnugRide infant seats. A disagreement could wind up in court if it proves contentious. In an e-mailed statement, Graco said it "identified that food and dried liquids can make some harness buckles progressively more difficult to open over time or become stuck in the latched position." The company is offering an improved replacement harness buckle to affected consumers at no cost. Graco also emphasized that the infant seats were not included in the recall, because they are "uniquely designed to detach from their base for quick release if needed." Those who have difficulty with an infant-seat buckle, however, should contact Graco and can also get a replacement buckle, Graco said. The child seat recall covers 11 models sold from 2009 through 2013. "Graco would like to stress this does not in any way affect the performance of the car seat or the effectiveness of the buckle to restrain the child," the company said in the statement. NHTSA says it has at least 80 complaints about the seats. Parents said they had to use excessive force to unlatch the harness buckle. In some cases, the straps had to be cut to free children. Graco said in a letter to NHTSA that it had been monitoring the performan! ce of the buckles since 2009 and had given owners advice on how to use and clean them, and offered replacement buckles. The recalled models include: Cozy Cline; ComfortSport; Classic Ride 50; My Ride 65; My Ride with Safety Surround; My Ride 70; Size4Me 70; Smart Seat; Nautilus; Nautilus Elite; and Argos 70. Child safety advocate Joseph Colella emphasized that the Graco seats should continue to be used. "Since this investigation is not related to crash protection, the affected car seats should still be used until the repair kits are available, but repairs should be made as soon as possible," said Colella. Consumers can contact Graco toll free at 800-345-4109 or at or consumerservices@gracobaby.com.

Popular Posts: FB Stock – Why Facebook Could Soar Another 18%FB Stock: Who Will Be the Facebook of 2024?Should I Buy FB Stock? 3 Pros, 3 Cons Recent Posts: Should I Buy CVX Stock? 3 Pros, 3 Cons Flood of New Domain Names Yields Few Investment Opportunities Should I Buy FB Stock? 3 Pros, 3 Cons View All Posts Chevron (CVX) has had a bad start to the new year, dropping 11% so far in 2014. For a company of its scale and stability, that’s a frighteningly big move.  It certainly didn’t help that the company announced a dismal fourth-quarter earnings report. Profits plunged by 32% to $4.93 billion, or $2.57 per share. In fact, the company missed Wall Street's revenue expectations by a whopping $9 billion. Given this performance, it is no wonder that CVX stock has been selling off like crazy. It certainly didn’t help that the company announced a dismal fourth-quarter earnings report. Profits plunged by 32% to $4.93 billion, or $2.57 per share. In fact, the company missed Wall Street's revenue expectations by a whopping $9 billion. Given this performance, it is no wonder that CVX stock has been selling off like crazy.

But might this be an opportunity to pick-up a solid blue chip at a discount — and one with a nice dividend, at that? Let's take a look at the pros and cons: CVX Stock Pros Efficient operator: CVX stock has benefited from huge scale, with operations that span mining, chemicals and power generation. Yet, among its peers, the company is standout in its efforts to find cost savings. Its earnings per barrel come to about $23.33, which is $5 ahead of companies like BP (BP), Royal Dutch Shell (RDS.A), Total (TOT) and ExxonMobil (XOM). But CVX the company is also one of the world's largest producers of Liquefied Natural Gas (LNG), which has benefited from strong growth in places like Asia and Europe. Besides, LNG has massive barriers of entry because of the substantial requirements for infrastructure, logistics and technology. Secular trends: According to the 2013 EIA International Outlook, spending on energy will grow by 45% over the next 20 years. While other sources of energy will get a higher share, like solar, it still is likely that fossil fuels will remain the largest market. Yet there's a good chance that prices will increase over time because of the difficulties of finding new supplies. By 2035, there will need to be 65 million barrels per day of new production. To gear up for this, CVX has invested huge amounts towards exploration in places like Australia, West Africa, Iraq and parts of South America. The company should also benefit from its expertise in dealing with harsh environments, such as deposits in remote places of the earth or deep-well drilling. Financials and valuation: Even with the Q4 slip, CVX stock remains a top performer. For 2013, cash flows from operations came to $35 billion. A key use of the cash has been for dividends. Consider that last year marked the 26th consecutive increase in the annual dividend payout. As of now, the yield is 3.6%. The valuation of CVX stock is also attractive, with a forward price-to-sales ratio of only 10X. CVX Stock Cons Complexities: Mega energy projects are not only expensive and time-consuming but also prone to severe problems. While CVX has strong platform and highly talented employees, the company still has faced many issues. A recent example is the $49 billion natural gas venture in Australia, which has been dogged with complications. The budget has ballooned as the company has had to deal with adverse weather, currency volatility and mounting labor costs. All of those factors will weigh on CVX stock. World economy: With the Federal Reserve "tapering" its easy monetary policy, there have been shockwaves across the global economy. What's more, there are signs that China is undergoing a deceleration. So if there is a worldwide slowdown, it is likely that there will be further pressure on oil prices, which will certainly crimp the results for CVX stock. The disarray in emerging markets is also having a huge impact on currencies, which could result in lower earnings as well. Production: CVX has been lagging on this front lately. Even with huge investments in exploration, it has been tough to find new reserves. The fact is that new sources of oil are generally in remote parts of the world or in places that have volatile political systems. In the latest quarter, Chevron's global oil-equivalent production came to 2.58 million barrels a day, down from 2.67 million in the year-ago period. If not solved, this lingering problems could really hurt CVX stock in the long run. Verdict on CVX Stock There's little doubt that Chevron had an awful quarter. But then again, other major oil operators have also had difficulties. Despite all this, CVX stock is in a good position. It has critical expertise in deep-well drilling and also lucrative businesses in categories like LNG. More importantly, over the long-term there will likely be steady increases in demand for energy. And yes, the valuation on CVX stock is attractive and so is the dividend, which has been like clockwork. So should you buy Chevron? Yes — for now, the pros outweigh the cons on CVX stock. Tom Taulli runs the InvestorPlace blog IPO Playbook. He is also the author of High-Profit IPO Strategies, All About Commodities and All About Short Selling. Follow him on Twitter at @ttaulli. As of this writing, he did not hold a position in any of the aforementioned securities.

Alamy I'm a firm believer in giving back. I received so much in both formal and informal education during my four years in college, I naturally want others to reap the same rewards I did. It's because of this that I think that if you're able to, you should not only give the your alma mater the gift of money, but also the gift of time. You might not think of it this way, but you should value your college diploma like a share of stock. Graduates should want to see their alma maters grow in stature, and one way to help out is by giving back. Unfortunately, not enough alumni are giving back to their colleges these days -- and it shows. Giving back with our money and our time helps support the next generation of students and alumni. When we give back to our colleges, that money goes toward research, scholarships, and new facilities, among other things. It helps increase the stature of the college, making it a better place. Our giving back also affects how employers, grad schools and others see our alma maters. 'Giving Back' Doesn't Have to Mean Money We often forget that our time is valuable and can be almost as important as any donation we make to our alma maters. Human capital is just as beneficial to the sustained vitality of a university and can be just as important, if not more, than purely financial support. Colleges and universities need both. When we give back to our alma maters, we get a sense of satisfaction in knowing that we're furthering the aims of the institution that did so much to educate us and give us a better life. Alumni typically give back to their schools in proportion to their own gratitude and success. There may be a correlation to poor giving and the realization that our undergraduate degree directly led to a portion of our success. But should this always be the case? One reason that colleges don't enjoy higher alumni giving is that their graduates often fail to connect the dots of their success to their alma mater. Giving Back Makes Us Sharper, Too Education is a never-ending process. We continue to learn even after we graduate. And nothing is often more apparent than when we give back to our alma maters. Rebecca Stilwell is president of O'More College of Design and a former managing director with Morgan Stanley. "I heard one of our best professors say that he loves teaching because it makes him sharper in his field," she says. "It keeps him current. And every great teacher will say they get more out of teaching than the students." What better way to stay relevant, sharp, and challenged than to spend time with your alma mater? Giving Back Helps Your Own Reputation Helping improve the stature of our alma maters can have a second- and third-order effect on our own lives and the perceived value of our own college diploma. Whether it's giving our money or our time, we should all want to see our alma maters thrive. Doing so can only help our own lot in life. "We all want to make the world a better place," Shari Fox, executive vice president of O'More College of Design. "By sharing our time and talent and money with colleges, we do a bit of good and can even change lives by helping a worthy student earn a college education." Karma and Networking It's hard to pinpoint where success comes from in our working lives. What about karma? Should that factor into our giving back? And how much does networking through our alma maters play into it? "[Colleges] need mentors for juniors and seniors and graduate students," says Rosemary Guzman Hook, a certified career consultant and owner of Hook the Talent. "They need speakers for career panels, they need photo ops and success stories from alumni." What about networking with the next generation? Giving back to your alma mater can also help you increase your own network, and there's no better place to start than with the students and alumni of your alma mater. "You should help your fellow alumni with whatever expertise or connections you can reasonably offer," says Hook. "You'll often get the same in return, and you may even become a recognized resource back at the school, which would open up a whole other wave of new contacts for you." Are You Giving Back to Your Alma Mater? Many of the benefits you get from college are intangible, and the things you give back aren't always easy to measure. But one thing is clear: America's colleges and universities today are in desperate need of both financial support and volunteer assistance from their alumni. And giving back now can provide you with dividends for years to come. Alamy I'm a firm believer in giving back. I received so much in both formal and informal education during my four years in college, I naturally want others to reap the same rewards I did. It's because of this that I think that if you're able to, you should not only give the your alma mater the gift of money, but also the gift of time. You might not think of it this way, but you should value your college diploma like a share of stock. Graduates should want to see their alma maters grow in stature, and one way to help out is by giving back. Unfortunately, not enough alumni are giving back to their colleges these days -- and it shows. Giving back with our money and our time helps support the next generation of students and alumni. When we give back to our colleges, that money goes toward research, scholarships, and new facilities, among other things. It helps increase the stature of the college, making it a better place. Our giving back also affects how employers, grad schools and others see our alma maters. 'Giving Back' Doesn't Have to Mean Money We often forget that our time is valuable and can be almost as important as any donation we make to our alma maters. Human capital is just as beneficial to the sustained vitality of a university and can be just as important, if not more, than purely financial support. Colleges and universities need both. When we give back to our alma maters, we get a sense of satisfaction in knowing that we're furthering the aims of the institution that did so much to educate us and give us a better life. Alumni typically give back to their schools in proportion to their own gratitude and success. There may be a correlation to poor giving and the realization that our undergraduate degree directly led to a portion of our success. But should this always be the case? One reason that colleges don't enjoy higher alumni giving is that their graduates often fail to connect the dots of their success to their alma mater. Giving Back Makes Us Sharper, Too Education is a never-ending process. We continue to learn even after we graduate. And nothing is often more apparent than when we give back to our alma maters. Rebecca Stilwell is president of O'More College of Design and a former managing director with Morgan Stanley. "I heard one of our best professors say that he loves teaching because it makes him sharper in his field," she says. "It keeps him current. And every great teacher will say they get more out of teaching than the students." What better way to stay relevant, sharp, and challenged than to spend time with your alma mater? Giving Back Helps Your Own Reputation Helping improve the stature of our alma maters can have a second- and third-order effect on our own lives and the perceived value of our own college diploma. Whether it's giving our money or our time, we should all want to see our alma maters thrive. Doing so can only help our own lot in life. "We all want to make the world a better place," Shari Fox, executive vice president of O'More College of Design. "By sharing our time and talent and money with colleges, we do a bit of good and can even change lives by helping a worthy student earn a college education." Karma and Networking It's hard to pinpoint where success comes from in our working lives. What about karma? Should that factor into our giving back? And how much does networking through our alma maters play into it? "[Colleges] need mentors for juniors and seniors and graduate students," says Rosemary Guzman Hook, a certified career consultant and owner of Hook the Talent. "They need speakers for career panels, they need photo ops and success stories from alumni." What about networking with the next generation? Giving back to your alma mater can also help you increase your own network, and there's no better place to start than with the students and alumni of your alma mater. "You should help your fellow alumni with whatever expertise or connections you can reasonably offer," says Hook. "You'll often get the same in return, and you may even become a recognized resource back at the school, which would open up a whole other wave of new contacts for you." Are You Giving Back to Your Alma Mater? Many of the benefits you get from college are intangible, and the things you give back aren't always easy to measure. But one thing is clear: America's colleges and universities today are in desperate need of both financial support and volunteer assistance from their alumni. And giving back now can provide you with dividends for years to come.

ST. LOUIS (AP) — As the Denver Broncos and Seattle Seahawks prep for their showdown in next weekend's Super Bowl, a legal fight is playing out over the turf installed months ago at the NFL title game's venue. Taylor Turf Installation is suing the MetLife Stadium's operators and the company that hired the suburban St. Louis company, seeking more than $292,000 that Taylor Turf claims it still is owed for hustling to install the New Jersey stadium's playing surface last summer. Taylor Turf's lawsuit in New Jersey's Bergen County Superior Court names New Meadowlands Stadium and Dalton, Ga.-based Turf Industry, doing business as UBU Sports. Turf Industry did not return Associated Press telephone messages seeking comment Friday. A MetLIfe Stadium spokeswoman said in an emailed statement that Taylor Turf's beef shouldn't be with the venue's operators, insisting New Meadowlands Stadium merely tapped the Georgia company to head the turf-installation project and has "no direct knowledge of the parties' contractual issues." "However, we have been in contact with UBU and have indicated that we expect them to resolve this matter quickly and amicably." the stadium's spokeswoman said. Taylor's president, Kelly Taylor, told the AP that his family-owned company has over the years laid the artificial playing surface in MetLife Stadium's predecessor in East Rutherford, N.J. — Giants Stadium — and several times in the Edward Jones Dome, home of the NFL's St. Louis Rams. Winning the deal for the 82,500-seat MetLife, with every major U.S. turf company having bid on the work, "was a huge deal," Taylor said. "We were beaming with pride, and we were all excited about the opportunity," he said. Given that the Super Bowl is a yearly global spectacle, this one being the first outdoors in cold weather, "we knew this field would be seen all over the world, so we gave it our best." Taylor Turf crews expedited the MetLife work, completing the $417,000 job last July in 11 days ! — roughly half the typical time requirement, Taylor said. But Taylor claims payments were slow in coming, saying his company was given $125,000 early in the project "to appease us" and that he was repeatedly assured more compensation was on the way. "All along, (chief contractor UBU Sports) kept saying, 'The payment's coming, but keep on working,'" Taylor said. "There should have been red flags from the beginning. At some point we should have stopped," stressing that "it doesn't matter how big or important this job is, we've got to get paid. But we didn't stop." Taylor concluded that the incessant demand by the project's overseers for paperwork "was just a stall tactic." "It's just a frustrating situation," said Taylor, whose decade-old turf-installation business is an offshoot of the Ambassador Floor venture that his father launched in 1985. It was not immediately clear Friday whether a court hearing on the lawsuit has been scheduled.

SAN FRANCISCO -- Expedia may have been hit by a "negative SEO" campaign that hammered the travel website's rankings on Google searches, according to an analysis by the firm that uncovered the problems. Expedia's website lost 25% of its visibility in Google search between Jan. 12 and 19, after Google clamped down on efforts to boost its online traffic through paid links from other sites, third-party search analytics firm Searchmetrics said on Monday. Expedia shares fell on Tuesday on concern about the impact to its business and the stock was down again on Wednesday. Searchmetrics Founder Marcus Tober completed a deeper analysis of the episode on Wednesday and shared the data and his conclusions with USA TODAY. The main take-away: The techniques used to increase Expedia's search visibility were so clumsy and out-dated - and used in such high volume - that it would be very surprising if the company alone was responsible for the scheme. Instead, Tober reckons there are three possible reasons for the scheme. First, Expedia may have used artificial link building techniques years ago and the company forgot that they did this and left the links on the web. Or, some department within Expedia, or a third-party hired by the company, is still using these out-dated techniques, Tober said. Expedia is a big company, with many search engine optimization, or SEO, teams that work with different agencies, so it is possible that one one rogue department was responsible. Lastly, an Expedia competitor built these links in the past, over a long time, to hurt Expedia, Tober said. This strategy, known as "negative SEO," has become more common in recent years, he noted. Dave McNamee, a spokesman for Expedia, declined to comment on Wednesday. Whatever the reason, Expedia's rankings in important travel-related search results have been hit hard. For example, in a Google search using the word "hotels" on Wednesday, Expedia's website appeared no where on the first few pages of resu! lts. In the past, expedia.com would have appeared in the number three spot on the first page, according to Tober. The word "hotels" was used more than 15,000 times as an anchor text on many websites to create links back to Expedia's main website, according to the Searchmetrics analysis shared with USA TODAY. In one example - http://www.vngarden.com/w/ - a website about traveling in Vietnam was created and at the bottom of the page it says "Designed by the Expedia Hotels Team." The word Hotels links to the hotel section of Expedia's main website. "This is very unusual and never done anymore in search," Tober said. "This is completely obvious to Google's search engine that these sites are made just for the links." In another example, a German-language blog - http://internet-maerchen.de/blog/ - was created. At the bottom, it says "Designed by the Expedia Cheapest Flights Team." This time, the link is to the flights section of Expedia's main website. However, the font used for this links is white on a white background, so most visitors to the site would not see the words and the link. Tober uncovered it by highlighting the area with his computer's cursor. "I don't know why Expedia did this. This is a technique that stopped about 10 years ago," Tober said. This adds to his suspicion that the episode may have been caused by negative SEO. "In the last year or two there has been a lot of movement within the black hat industry to use negative SEO to hurt rankings of companies with these kinds of techniques," he added. "Hopefully Expedia will recover soon."

This morning we are going to take a look at stocks that are widely held by the gurus and trading near their 52-week lows: eBay Inc. (EBAY) closed at $48.56 on 6/12/2014, near its 52-week low of $48.06. The company provides online platforms, tools, and services to help individuals and merchants in online and mobile commerce and payments in the United States and internationally. The company is facing stiff competition from Amazon and recent news stories indicate that Amazon and Apple will soon be competitors of their PayPal service. Activist investor, Carl Icahn (Trades, Portfolio), recently took a large stake in the company to help bring some life back into the stock. He was fighting for a spinoff of PayPal, and had a discussion with the CEO. After they met, Icahn backed off of his request, and is on board with the company's plans. It is currently held by 35 of the gurus we follow.

Market Cap: 61.54 billion, P/E: N/A Business Predictability: 4/5, Financial Strength: 8/10, Profitability & Growth: 8/10